About Us

Financial markets are undergoing an unprecedented transformation. Technological advances have brought major improvements to the operations of financial services, making them quicker, cheaper, and easier to access. Payment systems have become faster, investment advice is now offered algorithmically, and many borrowing/lending platforms are offering cheaper financing options than banks and credit card companies. Artificial intelligence (AI) techniques are having a profound impact on the design and efficiency of financial services, ranging from credit assessment to strategic forecasting, market governance, and regulation.

Now more than ever, we need to understand the potential of these technologies, integrate AI algorithms into customizable financial products and services, and assess the security mechanisms, and the economic implications of this transformation. The Center for Digital Finance and Technologies has been created with this purpose in mind, and through its various teaching, research, and outreach initiatives it aims to change the way academic institutions, regulators, and the private sector think. The Center leverages multi-disciplinary expertise at Columbia in diverse domains such as computer science, engineering, data science, finance, and economics, to answer these fundamental questions.

If you would like to receive updates about the Center's activities, please sign up here. You can unsubscribe from the list at any time.

CDFT Newsletter

November 2025

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

October 2025

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

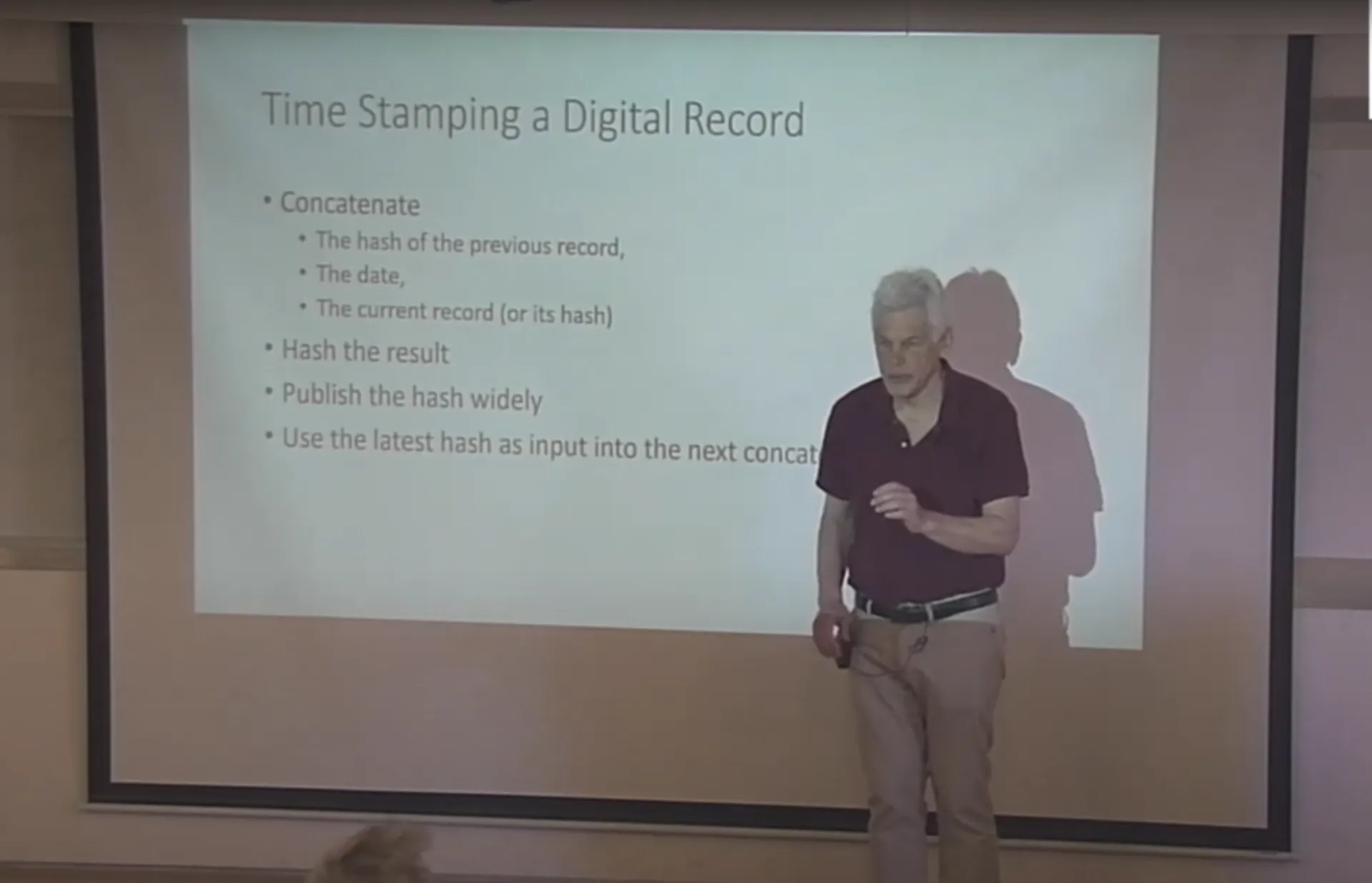

Overview of the digital transformation of financial services by Agostino Capponi. Slides available here.

An introduction to bitcoin and blockchain by Gur Huberman

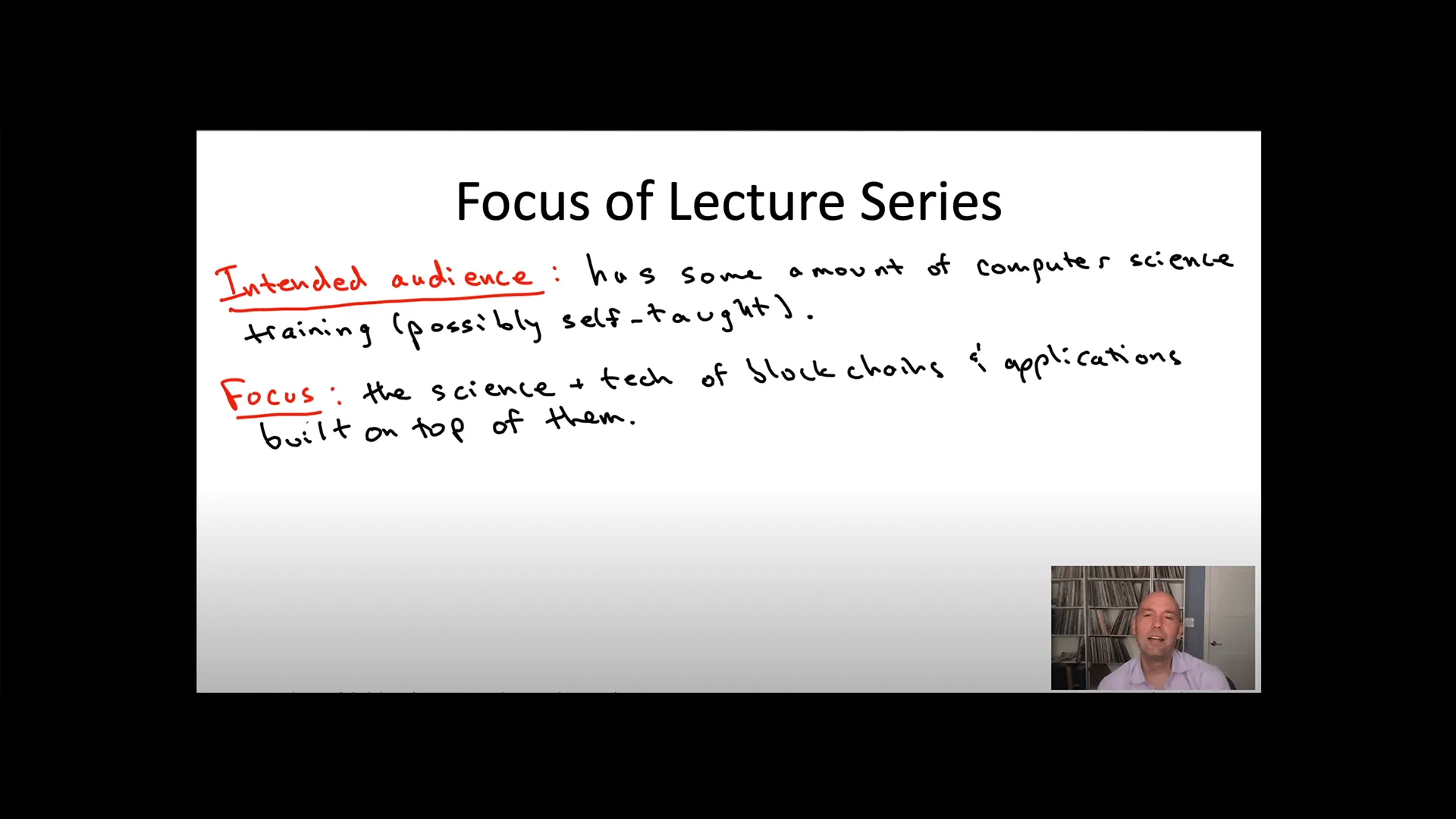

Foundation of Blockchain Lecture Series by Tim Roughgarden

Introduction to Blockchain Security and Vulnerability by Ronghui Gu